Featured

Table of Contents

Common methods consist of: Personal loansBalance move credit cardsHome equity loans or lines of creditThe goal is to: Lower interest ratesSimplify monthly paymentsCreate a clear payoff timelineIf the new rate is meaningfully lower, you reduce total interest paid. Many charge card use:0% initial APR for 1221 monthsTransfer charges of 35%Example: You move $10,000 at 22% APR to a 0% card with a 4% transfer charge.

This works well if: You qualify for the credit limitYou stop including new chargesYou pay off the balance before the advertising period endsIf not paid off in time, interest rates can leap dramatically. Benefits: Lower interest rate than credit cardsFixed month-to-month paymentClear payoff dateExample: Changing 22% APR credit card debt with a 912% personal loan significantly lowers interest expenses.

Utilizing home equity can provide lower rates of interest. This shifts unsecured credit card debt into protected debt connected to your home. Dangers: Failure to repay could threaten your homeExtending payment increases long-lasting exposureThis alternative requires caution and strong repayment confidence. Debt consolidation might be helpful if: You receive a considerably lower interest rateYou have steady incomeYou commit to not building up new balancesYou want a structured repayment timelineLowering interest accelerates reward however only if costs behavior modifications.

Before combining, calculate: Current average interest rateTotal remaining interest if settled aggressivelyNew interest rate and overall expense under consolidationIf the math plainly favors consolidation and behavior is controlled it can be strategic. Debt consolidation can momentarily affect credit history due to: Hard inquiriesNew account openingsHowever, over time, lower credit utilization often improves ratings.

Removing high-interest financial obligation increases net worth directly. Transferring balances however continuing spendingThis develops two layers of debt. Picking long payment termsLower payments feel easier however extend interest exposure.

2026 Analyses of Debt Management Programs

Closing accounts can increase credit usage and impact rating. Rates may not be significantly lower than existing credit cards. Credit card financial obligation combination can speed up benefit however just with discipline.

Automate payments. Combination is a structural enhancement, not a behavioral cure.

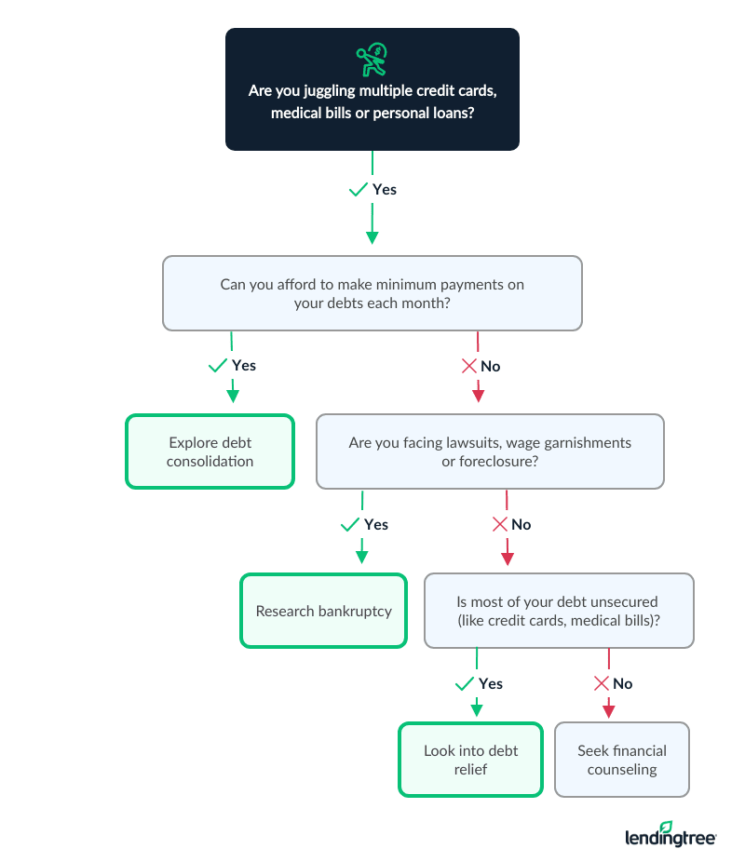

It can be intimidating when your charge card debt starts to surpass what you can pay, specifically since in some cases all it takes are one or 2 mistakes and soon you're managing several balances from month to month while interest starts to accumulate. Credit card financial obligation consolidation is one type of relief readily available to those struggling to settle balances.

Leveraging Debt Calculators for 2026

To leave the stress and get a deal with on the debts you owe, you require a financial obligation payment gameplan. In a nutshell, you're seeking to discover and gather all the debts you owe, find out about how debt consolidation works, and lay out your options based upon a complete evaluation of your financial obligation situation.

Balance transfer cards can be an excellent form of combination to think about if your financial obligation is concerning however not frustrating. By requesting and getting a new balance transfer credit card, you're basically purchasing yourself additional time generally someplace between 12 and 21 months, depending upon the card to stop interest from accumulating on your balance.

Compared to other combination alternatives, this is a reasonably easy method to understand and achieve. Lots of cards, even some rewards cards, offer 0% APR promotional durations with no interest, so you might be able to tackle your full debt balance without paying an additional penny in interest. Moving debts onto one card can also make budgeting easier, as you'll have less to track every month.

The majority of cards state that in order to benefit from the introductory advertising period, your financial obligation has actually to be moved onto the card in a particular timeframe, usually in between 30 and 45 days of being approved. Depending on the card, you might have to pay a balance transfer fee when doing so.

Essential 2026 Planning Calculators for Borrowers

Another word of caution; if you're unable to repay the quantity you've moved onto the card by the time to introductory marketing period is up, you'll likely go through a much greater rate of interest than previously. If you pick to progress with this method, do whatever in your power to ensure your financial obligation is settled by the time the 0% APR period is over.

This might be a good option to consider if a balance transfer card seems ideal but you're not able to fully devote to having the financial obligation paid back before the rates of interest starts. There are numerous individual loan choices with a variety of repayment durations offered. Depending upon what you're eligible for, you might have the ability to set up a long-term plan to settle your financial obligation over the course of several years.

Similar to stabilize transfer cards, individual loans may also have charges and high rate of interest connected to them. Often, loans with the least expensive rates of interest are limited to those with greater credit rating a task that isn't easy when you're handling a great deal of financial obligation. Before signing on the dotted line, make certain to evaluate the small print for any fees or information you might have missed out on.

By borrowing versus your pension, generally a 401(k) or IRA, you can roll your debt into one payment backed by a retirement account used as collateral. Each retirement fund has particular rules on early withdrawals and limitations that are important to examine before deciding. What makes this choice possible for some people is the lack of a credit check.

As with a personal loan, you will have several years to settle your 401k loan. 401(k) loans can be high-risk because failure to repay your debt and follow the fund's rules could irreparably damage your retirement cost savings and put your accounts at threat. While a few of the rules and policies have softened throughout the years, there's still a lot to think about and digest before going this path.

Using Debt Calculators for 2026

On the other hand, home and vehicle loans are classified as protected debt, due to the fact that failure to pay it back might mean repossession of the asset. Now that that's cleaned up, it is possible to consolidate unsecured financial obligation (credit card financial obligation) with a secured loan. An example would be rolling your charge card financial obligation into a mortgage, essentially collecting all of the balances you owe under one debt umbrella.

Safe loans also tend to be more lenient with credit requirements because the used property offers more security to the lending institution, making it less risky for them to provide you cash. Home mortgage in specific tend to use the biggest sums of cash; likely enough to be able to combine all of your credit card financial obligation.

{kind=link}

Latest Posts

Managing Loan Balances Plans in 2026

Ways to Obtain Competitive Financing for 2026

New 2026 Repayment Tools for Borrowers